There’s nothing wrong if we say that Health

Insurance should be purchased to “save your savings”. On one side there’s increase

in Life expectancy due to improvement in medical facilities and on the other

there’s deterioration in health due to life style changes. And accompanied with

increasing medical costs and other healthcare expenses, keeping one self

adequately insured with proper health insurance cover has become inevitable.

Though individuals start realizing the importance

of health insurance but still they are more confused with number of products

available in the market. Previously there were only general insurance companies

that provide this insurance, then came Standalone health insurance companies

and now Life Insurance companies has also started selling health insurance.

This confusion is clearly visible among people as, whenever any new plan is

launched in the market people gets excited and starts enquiring about the same.

Recently LIC has launched a new Health Insurance Plan naming “Jeevan Arogya”.

So, we have tried to review this from a Financial

Planning perspective and how does Jeevan Arogya stand against existing policies

in the industry.

Who can be insured under LIC Jeevan Arogya ?

Under a single policy you can cover your complete

family (which includes you, your spouse and children), your parents and your

parents –in-law.

The Minimum and maximum age at entry is as under:

|

Minimum age at entry

|

Maximum age at entry

|

|

|

Self/Spouse

|

18 years

|

65 years

|

|

Parents/Parents in law

|

18 years

|

75 years

|

|

Children

|

91 days

|

17 years

|

Features & benefits of LIC Jeevan Arogya

- LIC Jeevan Arogya is a defined benefit, non linked plan where the benefits are fixed and will be payable to you in full, irrespective of the actual amount spent on treatment.

- It covers the Hospital cash Benefit (HCB) which means that you will be paid a defined amount for the number of days you have stayed in the hospital. There are 4 variants available under this feature. Rs 1000 per day, Rs 2000 pr day, Rs 3000 per day and Rs 4000/- per day. Your premium and other features and sum assured will be dependent on the variant you have chosen under HCB.

- Jeevan Arogya covers some 140 defined major surgeries. In case you get operated for any surgery as defined under this policy feature you will be paid lump sum amount which is equal to 100 times the HCB chosen. Which means that if you have chosen a plan of Rs 2000/- per day HCB then your Sum assured under Major Surgical benefit (MSB) feature would be Rs 2 lakh. And this amount will be paid to you irrespective of your actual expenditure on the procedure.

- There is some 140 day care procedures defined under this plan. If you get operated under that specific procedure than you will be paid 5 times of HCB plan you have chosen. Which means if you have chosen a plan of Rs 2000/- per day HCB then your sum assured under day care Treatment feature would be Rs 10000/-. And this amount will be paid to you irrespective of your actual expenditure on the procedure.

- In the event of an Insured under this plan, undergoing any surgery not listed under MSB or day care treatment causing the insured hospitalization to exceed a continuous period of 24 hrs with in the cover period, then a daily benefit equal to 2 times the HCB shall be paid for each continuous period of 24 hrs.

Special Features of LIC Jeevan Aarogya

- Double benefit: If due to medical complications patient has to admit to ICU then he becomes eligible to claim 2 times of HCB as per the plan.

- Coverage for all: You can cover your Parents and Parents-in-law under the same single policy along with you, your spouse and children.

- Quick Cash Facility: Though this is a Reimbursement policy which means that you have to make claim of the policy benefits after getting the treatment done. But in special surgeries covered under MSB, insured can claim 50% of the Sum assured which may be paid during hospitalization period. This amount will be adjusted in the final settlement.

- Premium Waiver benefit: In case the procedure operated under special categories defined under the MSB then one year premium will be waived.

- Riders : There are 2 additional riders offered under the policy- Term assurance rider under which the maximum sum assured offered is 100 times of HCB and Accident benefit rider where the sum assured offered should be less than or equal to Sum assured under Term assurance rider.

Limitations of Jeevan Arogya

In this we’ve not covered the basic and general

limitations and exclusions that are applicable to almost all the Health

Insurance policy. But specific limitations as is there in the features of the

policy.

- There’s annual and Lifetime limit imposed on the Daily cash benefit feature in LIC Jeevan Arogya. In the first year one cannot claim for more than 30 days in case of NON ICU stay and for ICU stay the LIMIT is 15 days. Second year onwards this limit will be increased to 90 days for NON ICU stay and 45 days for ICU stay. In lifetime you can claim maximum of 720 days in case of NON ICU stay and 360 days in case of ICU stay.

- In Major surgical benefit you can claim only once in one year and 8 times in lifetime.

- In day care Procedures you can claim maximum for 3 procedures in a year and limit is 24 for lifetime. Also, it’s not paid if you claim for Hospital Cash Benefit

- For Term assurance rider your Total Sum assured from other policies and riders should not exceed 25 lakh.

- For accidental Rider your total sum assured under all other individual and group policies should not exceed Rs 50 lakh.

- Maximum Sum Assured in the policy is Rs 4 lakh.

Complications in LIC Jeevan Arogya

Here we’ve covered those limitations which

usually gets hide under the noise of benefits but comes to cover at the time of

claim. As the Policy is Reimbursement policy so one must know what to be

claimed for otherwise this will lead to unnecessary harassment afterwards.

- If both of the parents (father and mother) are alive and are eligible for cover, then either both of them will have to be covered or none of them will be covered. The PI will not have any option to choose one of them. The same condition will apply for parents-in-law also.

- All the benefits will become payable only if the Hospitalization or surgery has been performed in India

- If more than one major surgery is performed during the same surgical session, you can claim for only one surgery.

- If more than one day care procedure is performed during the same surgical session then you can claim for only one procedure.

- No benefit will be paid for first 24 hrs of stay in the hospital. Which means that if your stay in Hospital is for 5 days , you will be paid for only 3 days. But if your stay exceeds 7 days then afterwards you become eligible to be paid for first 24 hrs also.

- The HCB will be paid for continuous stay of 24 hrs in Hospital or part there of provided any such part exceed continuous period of 4 hrs ( after having completed 24 hrs as above).

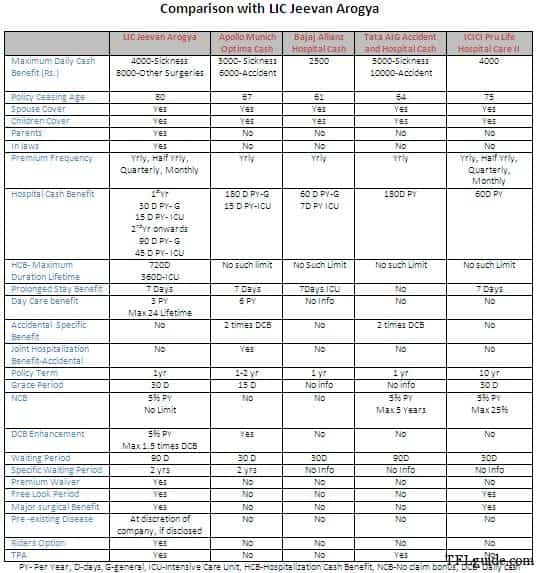

Comparison of LIC Jeevan Arogya with other Health Insurance Policies

If you draw a comparison between existing

policies from Apollo Munich, Bajaj Allianz and Star Health, you find these much

simpler in terms than LIC. Also the desired benefits which an individual seeks

from the policy are higher in certain areas.

Should you buy Lic Jeevan Arogya

Health insurance is a very specialized field and

requires a good amount of knowledge to understand the jargons a company uses in

the policy terms. LIC is a life insurance company and whether agents have

equipped themselves to sell these kinds of product, time will tell. In the case

of Reimbursement policies and that too from nationalized companies, role of

agent increases as they don’t have the culture of customer service centers/ 24

hr service numbers.

Though LIC has tried to bring

in life and health benefits together through this product. This has only

introduced complexity in the mind of consumers especially in areas

where financial literacy is too low.

With regard to LIC Jeevan Arogya

– it cannot be considered as an adequate health insurance policy as it does not

cover actual hospitalization cost. Also the maximum SA of Rs 4 lakh available

only in the case of major surgeries which in turn is too low for treatment

costs related to heart, kidney or stroke etc. However, if you are adequately

insured through other Health insurance policies but want to get cover of

additional expenses like room attendant costs, expenses on food, travelling

etc, then you can consider such policies. But again that insurance policy needs

to be simpler. Now days many Health insurance providers have added Daily cash

benefit feature with other benefits in their basic plans. Hence, our

recommendation is to evaluate your needs first and after comparing the policy

benefits in details (check policy wordings) with your basic policy, make your

decision. Unawareness on terms of the policy can lead to dissatisfaction to

your family during the claim settlement.

If you have any questions related to Health

Insurance – feel free to ask. contact us

~

Source : tflguide

{kind=link}

No comments:

Post a Comment